Quarterly International Carbon Update: Q2 2026

A curated selection of key developments, emerging trends, and market updates from the past quarter that deserve a place on your reading list.

The second quarter of 2026 has brought significant developments across the global climate and energy landscape, from record-breaking renewable energy milestones and evolving corporate climate strategies, to the growing challenges posed by extreme weather and the rapid expansion of AI infrastructure.

In this quarterly update, we explore the latest international carbon emissions trends, examine how climate finance is being strategically directed for maximum impact, and highlight the key policy, technology, and market developments shaping the transition to a low-carbon future.

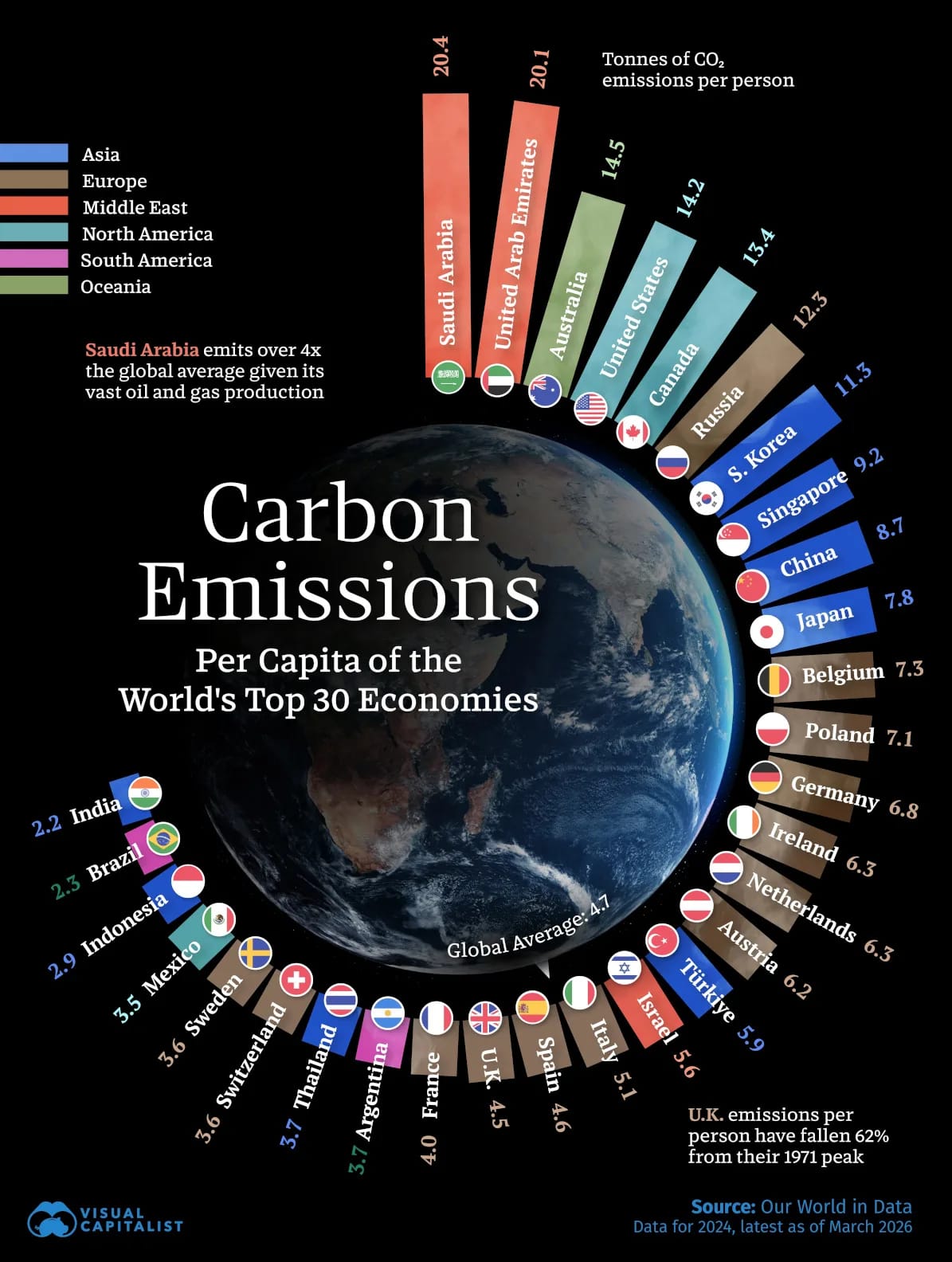

Which Countries Emit the Most CO2 Per Person?

The graphic above, which uses the latest figures from Our World in Data, ranks the CO2 emissions per capita of the world’s top 30 economies by GDP, measured in tonnes per person in 2024.

While global average CO2 emissions remain below five tonnes per person, the gap between countries is striking, with some emitting nearly 10x more per person than others. Factors such as energy production, industrial activity, economic structure, population size, and access to natural resources all play a major role in determining per-capita emissions, and highlight the uneven challenges countries face on the path to decarbonisation.

Saudi Arabia and the United Arab Emirates each generate more than 20 tonnes of CO2 per person annually, placing them among the world's highest per-capita emitters. Their high emissions are largely driven by fossil fuel dependence, energy-intensive industries, and relatively small populations.

Australia, the United States, and Canada also rank among the largest per-capita carbon emitters, producing around three times the global average. Resource-heavy industries, extensive energy consumption, and transport demands all contribute to their significant carbon footprints.

In Europe, Russia remains the region's largest major economy emitter on a per person basis, producing 12.3 tonnes of CO2 per capita due to its extensive energy production sector.

Across Asia, CO2 emissions per capita vary considerably. South Korea leads the region with 11.3 tonnes per person, reflecting its strong manufacturing and industrial base. Singapore records 9.2 tonnes per capita, supported by its role as a global oil refining and trading hub. China emits 8.7 tonnes per person – almost double the global average – but is also investing heavily in clean energy technologies, including solar power, electric vehicles (EVs), and green hydrogen. And India produces 2.2 tonnes of CO2 per person. While coal remains a key part of its energy mix, the country has exceeded major solar energy targets and is rapidly expanding renewable energy capacity, with plans to triple capacity by 2030 compared with 2022 levels.

How Climate Triage Allocates Capital for Maximum Impact

To achieve ambitious global climate goals, major philanthropic initiatives are moving away from broad, equal funding models in favour of a data-driven triage approach. Rather than distributing resources evenly, this model prioritises heavy-emitting countries with existing regulatory capacity to rapidly transition their electricity grids to solar and wind power, where targeted investment can deliver the greatest and fastest reductions in carbon emissions before critical climate deadlines.

Bloomberg Philanthropies' recent $285 million commitment to expand clean energy industries across emerging and developing economies demonstrates this strategy in practice. These economies collectively account for nearly 70% of global power sector emissions, making them a crucial focus for climate finance. By directing funding towards countries with the greatest potential for rapid decarbonisation, the initiative supports the global ambition for these economies to generate more than half of their electricity from renewable sources by 2030.

“Clean energy is now cheaper than fossil fuels in virtually every part of the world, and as a result, its share of global power production is growing. But fixable obstacles are still slowing down deployment – and with energy demand rising at an unprecedented speed, we can’t allow those obstacles to continue standing in the way of lower energy costs for households and businesses, and cleaner air and water for communities. This new investment will help ensure they don’t.”

– Michael Bloomberg, UN Special Envoy on Climate Ambition and Solutions, and founder of Bloomberg L.P. and Bloomberg Philanthropies

Four Core Criteria for Evaluating Country Profiles

When assessing where climate finance can have the greatest impact, organisations typically evaluate four key factors:

1. Emissions reduction potential – the extent to which renewable energy can displace existing fossil fuel generation.

2. Regulatory readiness – the presence of supportive policies, streamlined permitting processes, and legal certainty for investors.

3. Grid bottleneck severity – whether targeted investment can quickly improve transmission infrastructure and unlock additional renewable energy capacity.

4. Capital leverage mobilisation – the ability of early-stage funding to attract significantly larger investments from private markets and development institutions.

Four Strategic Funding Tiers

- Tier 1: Large, high-emitting economies with strong deployment potential

- Tier 2: Fast-growing emerging economies where future emissions can be avoided

- Tier 3: Wealthy high per-capita emitters where policy and technology shifts can demonstrate global leadership

- Tier 4: Smaller nations with high innovation potential that can serve as climate testbeds for scalable solutions

Headline News: Global

21 May 2026: The Science Based Targets initiative (SBTi) unveiled its SBTi 2026–2030 Strategy, marking a fundamental shift from merely validating climate goals to becoming a comprehensive transition partner.

"The world has changed significantly since the SBTi was established 10 years ago... The rationale for setting targets has evolved. Science-based targets are now a means to manage transition risk, strengthen business resilience, remain competitive, and create value in a carbon-constrained world. Evidence suggests that companies with targets benefit from increased strategic focus, efficiency gains, strengthened investor and customer perception, and faster emissions reductions compared to companies without targets. We have listened to feedback from companies and partners and will maintain the SBTi’s widely recognised status as the ‘gold standard’ for corporate climate action, evolving our approach through four major shifts..."

These four shifts are organised under two core dimensions: Ambition to Action (shifts 1 and 2) and Maximising Impact (shifts 3 and 4).

- From generalised to tailored approaches: While the first phase of the SBTi used a generalised approach, the new strategy moves toward sector-specific and geographic approaches. These tailored methods will be based on what companies can actually influence and will ensure they work alongside other existing frameworks.

- From ambition to implementation: Building on its success in getting thousands of companies to set targets, the SBTi is now pivoting toward implementation. This shift includes a stronger emphasis on data transparency and assessing progress and challenges at a system-wide level.

- Strengthening partnerships: To address fragmentation in the climate ecosystem that often leads to duplicated efforts and extra burdens for businesses, the SBTi will strengthen its partnerships to ensure more "joined-up" and coherent approaches.

- Expanding emissions coverage: The SBTi aims to maximise its impact by expanding its network. This includes targeting growth in high-emitting regions (such as establishing offices in India and South-East Asia) and focusing on high-emitting sectors and corporate supply chains.

Ultimately, the strategy seeks to bridge the gap between corporate ambition and measurable action to meet urgent global climate objectives.

7 April 2026: When scientists try to model how hot Earth could get this century, they typically look at a range of possibilities for how much planet-warming pollution humans might pump into the atmosphere. These scenario frameworks are periodically updated to reflect advances in climate science, emissions trends, and policy developments.

The publication of CMIP7 (ScenarioMIP-CMIP7) – the latest Scenario Model Intercomparison Project (ScenarioMIP) framework – establishes seven core scenarios, spanning futures from limited climate action and high emissions to ambitious mitigation pathways consistent with the Paris Agreement.

A significant innovation in this phase is the shift toward emissions-driven simulations, allowing models to better account for uncertainties in the carbon cycle and climate feedbacks. The framework also incorporates long-term extensions up to the year 2500 to study climate reversibility and the stability of the Earth system over multi-century timescales.

Notably and positively, the new ScenarioMIP framework no longer includes the very high-emissions RCP8.5 pathway. Many climate scientists now regard RCP8.5 – which has been prominently cited in thousands of climate studies over the past decade – as an increasingly implausible reference scenario in light of current energy trends and climate policies.

Headline News: EMEA (Europe, Middle East, & Africa)

June 2026: With heatwaves sweeping across the UK and much of Europe, some of the roughly 1,000 events scheduled for London Climate Action Week (LCAW) had to be cancelled or adapted due to a Red Extreme Heat Warning issued by the Met Office (the UK’s national meteorological service), which indicated a significant risk to health and life.

Organisers and attendees noted the irony that a major climate conference was itself being disrupted by the very challenges it had convened to address. Rather than discussing future climate impacts in the abstract, delegates found themselves experiencing them first-hand.

Impact of the Heatwave on Indoor Venues

London possesses a vast stock of Victorian, Georgian, and Edwardian buildings constructed from high-thermal-mass materials. While heavy masonry can moderate indoor temperatures over a typical day–night cycle, prolonged heatwaves combined with warm nights prevent these buildings from releasing the heat they have absorbed. As a result, heat accumulates over successive days, causing indoor temperatures to rise. Without sufficient ventilation, shading, or cooling, these buildings can become increasingly uncomfortable and, in extreme cases, hazardous for occupants.

At the other end of the spectrum are London's many modern glazed buildings. If poorly shaded or inadequately ventilated, they can experience substantial solar heat gain and are particularly prone to overheating during heatwaves. Without effective measures to limit or remove excess heat, indoor conditions can quickly become uncomfortable and, in severe cases, unsafe for occupants.

“Much of London’s building stock cannot function.” – Nick Mabey, CEO of climate campaign think tank E3G, and founder of London Climate Action Week

Impact of the Heatwave on Train Travel

During the heatwave, rail operators issued service disruption notices across England, Scotland, and Wales, warning people to "only travel if absolutely necessary". Eurostar also had to cancel several international trains departing London for Paris and Brussels due to the extreme heat on the network.

To fully appreciate how a heatwave can paralyse a modern rail network, it's helpful to understand the unique physics of steel rails and how track temperatures are managed by engineering teams.

Much of Britain's railway network was designed for a cooler climate, and critical infrastructure that once coped comfortably with summer conditions is now being tested by temperatures outside its original design envelope.

When ambient air temperatures reach 30°C, direct, intense sunlight can bake the dark steel rails to over 50°C, causing the metal to expand rapidly and exert immense physical pressure on the surrounding concrete sleepers and ballast. If the resulting compressive forces become too great, it can lead to dangerous physical deformation – a phenomenon known as buckling – which warps the track alignment and creates an immediate risk of a train derailment.

When rail temperatures approach critical thresholds, engineers use monitoring systems to assess conditions and impose temporary speed restrictions where necessary. Trains operating at slower speeds exert significantly less physical force on the warped rails, reducing the likelihood of a heat-stressed track deforming further under load.

In addition to buckled tracks, heatwaves also affect the overhead line equipment that supplies electricity to trains. These lines are engineered with counterweights to maintain a constant tension, but extreme air temperatures can cause the copper wires to expand and sag significantly. Excessive sag increases the risk of a train's roof-mounted pantograph (the arm that collects electricity from the overhead line) snagging the wire, physically tearing down the electrical infrastructure and cutting power to an entire route until repairs can be made.

“Extreme heat can have a significant impact on the railway.” – Jake Kelly, deputy CEO of Network Rail

Headline News: AMER (North, Central, & South America)

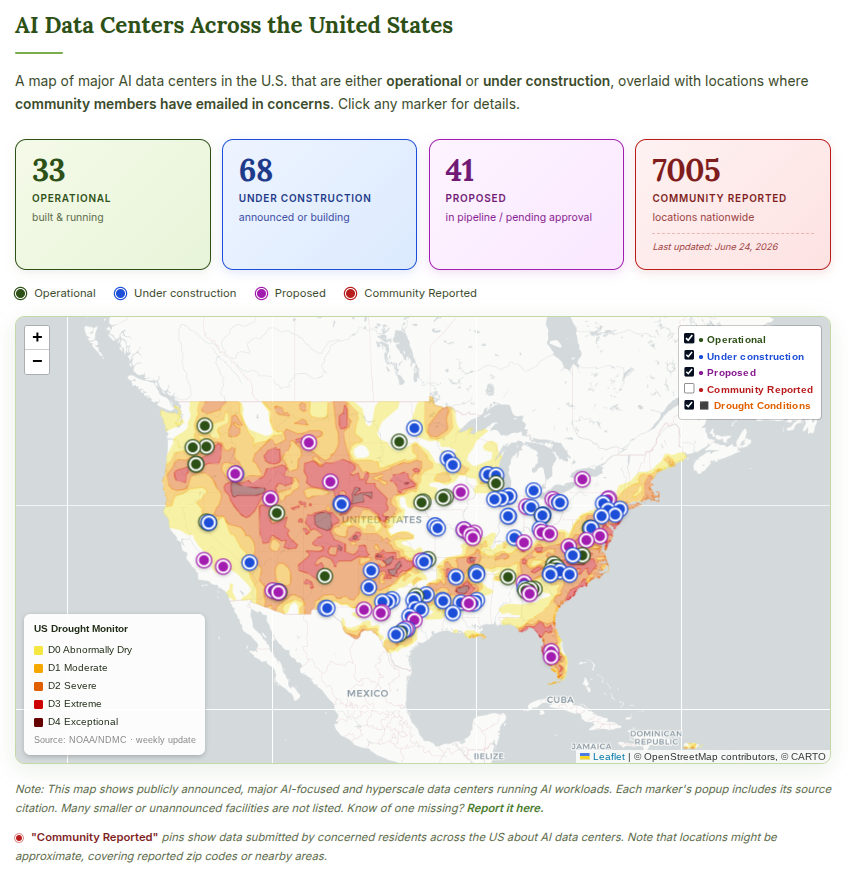

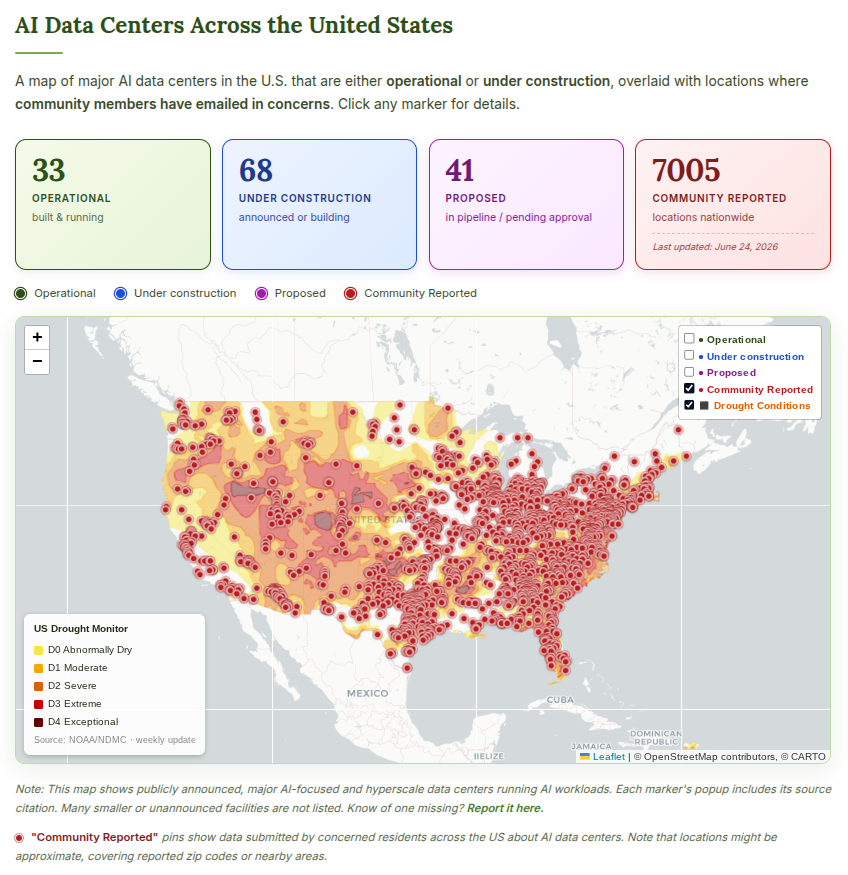

27 April 2026: American paralegal, consumer advocate, and environmental activist Erin Brockovich launched the Brockovich AI Data Center Reporting initiative, to track the rapid expansion of AI data centres across the United States after hearing growing concerns from communities about rising electricity demand, water use, noise pollution, and the strain on local infrastructure.

Pins on the website's interactive map labelled 'Operational', 'Under Construction', or 'Proposed' show publicly announced, major AI-focused and hyperscale data centres running AI workloads. Many smaller or unannounced facilities are not listed.

Pins labelled 'Community Reported' indicate verified submissions by concerned residents about AI data centres in their local areas.

The strain on local water supplies and ecosystems caused by these facilities – which often require substantial water resources to operate – is of particular concern in regions experiencing drought conditions.

In an article titled If Data Centers Are So Great, Why Are They Being Built in Secret?, Brockovich argues that "we have a transparency problem when it comes to data center construction".

“I want to be clear. I’m not making a blanket argument against data centers or against the technology they support. Some communities have welcomed these facilities after genuine public engagement, honest disclosure of impacts, and real negotiation of community benefits. When that happens, that’s democracy working the way it should.

What is not acceptable is the pattern our map documents: projects announced after permits are already secured, developers who don’t return calls, local officials who signed NDAs before their neighbors knew a project was being considered.

A company can be planning something the size of lower Manhattan in your county, drawing more electricity than a major American city, backed by hundreds of billions in borrowed money, and the people who live there may have no idea it’s coming until the trucks arrive.”

– Erin Brockovich

For the AI data centre industry – not just in the US, but globally – long-term success will depend not only on technical innovation, but also on social licence. The companies that thrive will be those that can demonstrate how their growth supports local communities, contributes to cleaner energy systems, and creates shared value.

Headline News: APAC (Asia & Pacific)

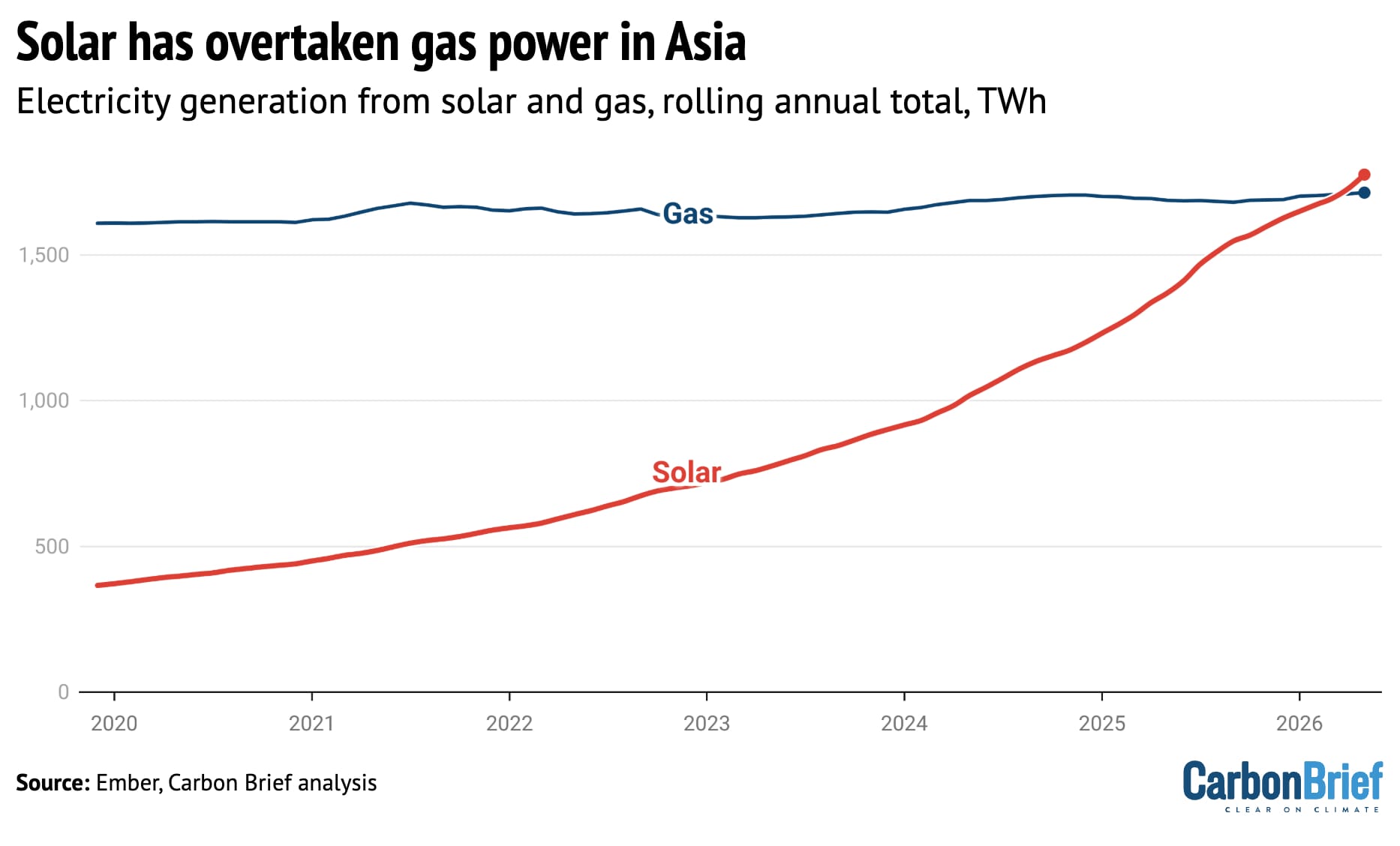

12 June 2026: Solar power has become Asia's third-largest source of electricity, overtaking natural gas for the first time ever. Over the 12 months to April 2026, solar generated around 1,727 terawatt-hours (TWh) of electricity, narrowly exceeding gas at 1,711 TWh.

The main driver has been the rapid growth of solar installations in China, supported by the country's large-scale manufacturing of affordable solar panels. Other countries, including India and Pakistan, have also seen strong growth as falling technology costs have made solar one of the cheapest ways to generate electricity. Since 2020, solar generation across Asia has nearly quadrupled, with the region accounting for around 60% of global solar growth.

At the same time, natural gas has become a less attractive option for electricity generation. Many Asian countries depend on imported liquefied natural gas (LNG), leaving them exposed to volatile prices and supply risks. Delays to new gas projects and rising costs have also slowed the expansion of gas-fired power.

Final Thoughts

The world already has the technology, investment pathways, and policy frameworks needed to reduce emissions at scale. What is needed now is rapid implementation where it will have the greatest impact, turning climate ambition into measurable progress.

If you found this analysis interesting, be sure to subscribe to our quarterly LinkedIn Newsletter. Our next Trends Report will be published at the end of Q3 2026.