Quarterly International Carbon Update: Q1 2026

Energy risk and resilience take centre stage as global markets and policy shifts impact net zero ambitions in Q1 2026.

We have entered the second half of a turbulent decade, and the global energy transition has entered a new, more uncomfortable phase – one where ambition is no longer the only variable.

A recent proposal by New York Governor Kathy Hochul to delay key climate targets in New York highlights a growing reality: decarbonisation is colliding head-on with the economic pressures of the ongoing energy crisis – which Fatih Birol, executive director of the International Energy Agency (IEA), has described as the biggest threat to global energy security in history.

What was once framed as a race toward net zero is increasingly becoming a balancing act between climate ambition, energy security and cost affordability. Rising energy costs, supply chain disruptions, and higher financing rates have exposed a critical vulnerability in transition planning – the assumption that decarbonisation would remain steadily cost-effective and politically frictionless.

This shift is not isolated. Across global markets, the aftershocks of inflation, geopolitical instability, and volatile fossil fuel prices are reshaping how governments approach climate policy. The energy crisis has underscored just how dependent modern economies remain on conventional energy sources, and how difficult – and expensive – it is to replace them at speed. As households and businesses absorb higher energy bills, the political appetite for aggressive, near-term climate costs is changing. The result is a subtle but significant pivot: from rapid decarbonisation at any cost, to what appears to be a more measured, cost-conscious transition.

At its core, this moment reflects a deeper structural tension. The benefits of climate action are long-term and widely shared, but the costs are immediate and highly visible. This imbalance is now playing out in policy decisions, where governments are being forced to reconcile environmental commitments with economic and political realities. The energy crisis has not diminished the urgency of climate action – but it has made clear that the pathway to net zero is far more complex, and more contested, than previously assumed.

For organisations navigating this landscape, the implications are profound. The era of linear, predictable decarbonisation is giving way to one defined by uncertainty, trade-offs, and shifting timelines. In this environment, resilience, flexibility, and data-driven decision-making will be just as critical as ambition.

Headline News: Global

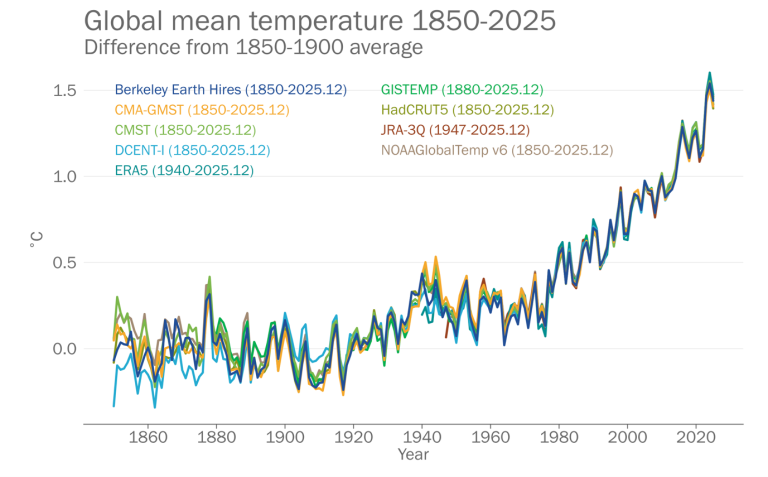

23 March 2026: In its State of the Global Climate 2025 report, the World Meteorological Organization (WMO) reveals that 2015–2025 were the hottest 11 years on record.

“Humanity has just endured the eleven hottest years on record. When history repeats itself eleven times, it is no longer a coincidence. It is a call to act. The State of the Global Climate is in a state of emergency. Planet Earth is being pushed beyond its limits. Every key climate indicator is flashing red.” – António Guterres, UN Secretary-General

Extreme events around the world, including intense heat, heavy rainfall, and tropical cyclones, caused disruption and devastation and highlighted the vulnerability of our inter-connected economies and societies.

The ocean continues to warm and is the dominant reservoir for excess heat in the climate system – storing more than 90% of the surplus energy caused by rising greenhouse gas (GHG) concentrations. Over the past two decades, the rate at which the ocean has warmed corresponds to energy absorption at roughly the equivalent of ~18x annual human energy use each year. The ocean also continues to absorb CO2 from the atmosphere – helping to partially offset atmospheric CO2 increases, though this drives ocean acidification and has impacts on marine ecosystems.

Arctic sea ice extent in 2025 was at or near record lows in the satellite era. And Antarctic sea ice extent was the third lowest on record. Glaciers and ice sheets globally have continued to lose mass unabated, contributing to rising sea levels.

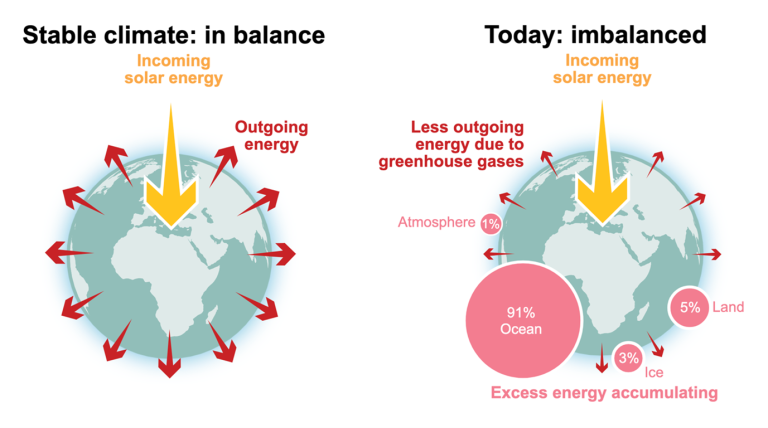

For the first time in its reporting, the WMO included data on Earth's energy imbalance (EEI) – a key climate indicator that measures how fast the heat trapped by anthropogenic emissions of GHGs is accumulating in the climate system.

If the amount of energy the Earth receives from the Sun (incoming solar radiation minus reflected solar radiation) exceeds the amount of energy the Earth radiates back into space (outgoing long-wave radiation), e.g. due to the greenhouse effect, the EEI is 'positive', meaning the Earth is gaining energy, mostly in the form of heat. If more energy escapes the Earth than is received, e.g. after large volcanic eruptions, the EEI is 'negative', meaning the Earth is losing energy, and cooling.

Due to increasing concentrations of GHGs, the EEI has become increasingly positive over time. Approximately 91% of surplus energy has been absorbed by the ocean, 5% by the continents, 3% by the cryosphere, and 1% by the atmosphere.

Not only has the EEI been increasing since 1960, when the observational record began, but the total amount of heat stored is accelerating, particularly in the past 20 years compared to the previous 66 years. In 2025, the observed EEI reached its highest value yet.

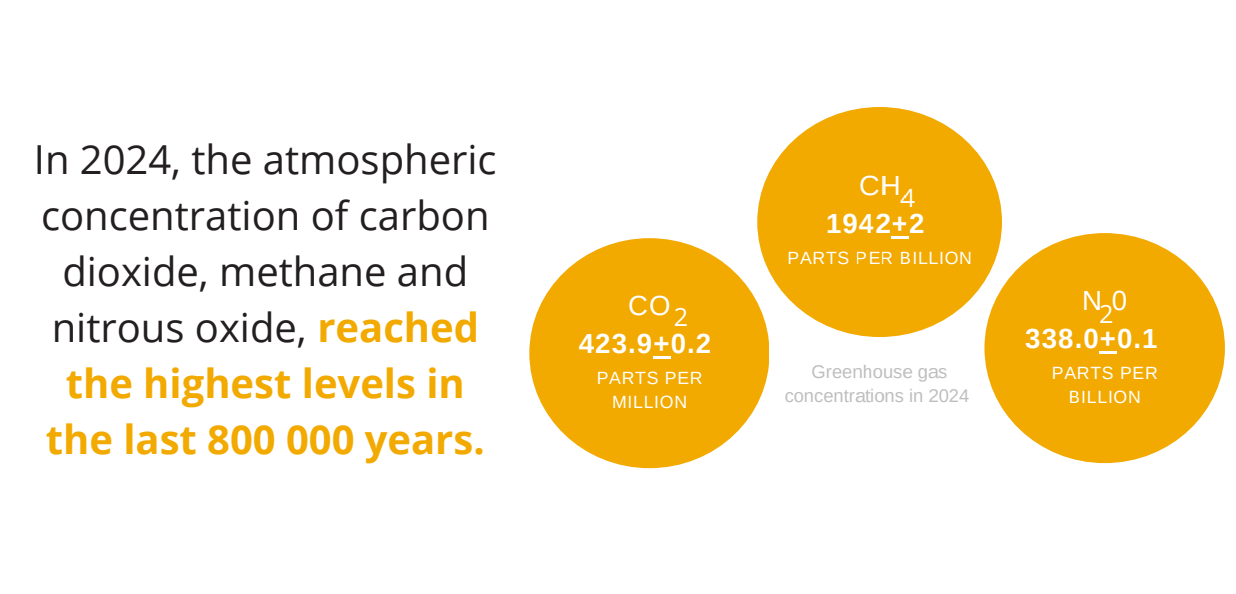

Data from individual monitoring stations show that levels of three main GHGs – CO2, methane, and nitrous oxide – continued to increase in 2025. And in 2024 – the last year for which we have consolidated global observations – the atmospheric concentration of these GHGs reached the highest levels in the last 800,000 years.

29 January 2026: The International Public Sector Accounting Standards Board (IPSASB) released its finalised IPSASB SRS 1, Climate-related Disclosurers standard. It is structured similarly to IFRS S2 – the IFRS Foundation’s International Sustainability Standards Board (ISSB) standard used in the private sector – but is tailored for the public sector.

Governments are major players in climate action, and until now there wasn’t a clear global set of rules on how they should report climate risks, opportunities, and related financial information. This standard gives a consistent way for public bodies to share that information. It focuses on how governments and public institutions should report on governance, strategy, risk management, metrics, and targets. The World Bank Group backed the development of this standard to help improve transparency, accountability, and decision-making in the public sector on climate matters.

Initially, the standard will not require government entities to report on the impact of their public policy programmes (e.g. national climate programmes and their results). That part is planned for a later update. And there are transition rules to make it easier to start reporting – for example, governments do not have to disclose Scope 3 emissions for the first three years, and they have some flexibility in how they report early on. In many places, governments would start using this for reports covering periods from 2028 onward, though early adoption is allowed.

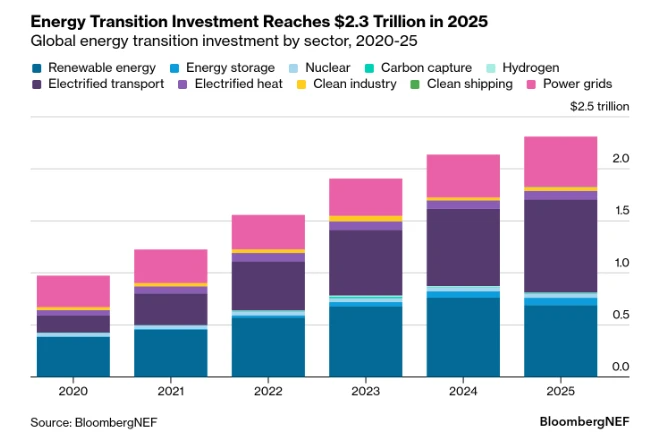

26 January 2026: In its annual Energy Transition Investment Trends report, BloombergNEF (BNEF) reveals that global investment in the low-carbon energy transition hit a new high in 2025, reaching US $2.3 trillion, up around 8 % year‑on‑year, despite persistent geopolitical and trade challenges. This figure includes spending to deploy clean technologies, build out low‑carbon infrastructure, equity raises for climate tech, and debt issuance – all of which rose over the year, highlighting a resilient pivot toward decarbonisation even amid market headwinds.

Electrified transport remains the standout driver of this growth, with ~$893 billion poured into electric vehicles and charging infrastructure. Renewables continues to attract substantial capital (~$690 billion), though renewable energy investment declined slightly in 2025 due to shifting policy environments in China, particularly in solar and wind markets. Meanwhile, investment in power grids climbed strongly, underscoring global efforts to strengthen networks for higher shares of intermittent generation and electrification.

Regionally, Asia‑Pacific remains the largest market, accounting for nearly half of all energy transition investment, with China still the single biggest investor, although its renewables spending dipped in 2025. The EU and India also showed solid growth, and even in jurisdictions with weakening policy support (like the US), clean energy investment continued to rise. These trends reflect an ongoing global diversification of capital flows and an expanding footprint of transition technologies worldwide.

At the same time, the broader investment picture shows that although clean energy capital now slightly outpaces fossil fuel supply investment, the pace of growth has slowed from double‑digit gains earlier in the decade to more modest annual increases. BNEF’s base‑case outlook anticipates average annual investment accelerating toward roughly $2.9 trillion through 2030 – a trajectory that, while encouraging, still falls short of what’s broadly considered necessary to align with net‑zero pathways.

21 January 2026: Microsoft argues that cutting emissions is essential but no longer sufficient; the world also needs carbon dioxide removal (CDR) at massive scale to stay within climate limits. To help build this nascent market, the company is using long-term purchasing commitments as a demand signal, with FY 2025 agreements covering 45 million tonnes of CO2 removal from 21 suppliers across multiple countries. This is central to the company's plan to be carbon negative by 2030 and to remove all historic emissions by 2050, with CDR reserved for residual and past emissions after aggressive reduction efforts.

Instead of betting on a single silver bullet, Microsoft is backing a portfolio of high-integrity solutions, from soils and rocks to forests and bioenergy. Examples include enhanced rock weathering with Lithos Carbon, which spreads finely ground basalt on farms to lock away CO2 for thousands of years while improving soil health, and Agoro Carbon Alliance, which helps farmers adopt regenerative practices that turn fields into reliable carbon sinks. On the engineered side, Microsoft has signed major offtake deals with Stockholm Exergi's BECCS (Bioenergy with Carbon Capture and Storage) project in Sweden, and with Brazil’s re.green, which restores diverse native forests using advanced monitoring, drones, and AI.

Across all of these projects, Microsoft emphasises rigorous measurement, verification, and community safeguards as the backbone of credible CDR. Contracts are structured so credits represent real, additional, and durable removals, tracked in registries to avoid double counting, while supplier support helps early-stage projects reach bankability and scale.

However, even with this rapid growth, today’s CDR volumes sit far below the estimated 7–9 billion tonnes per year needed by 2050, underscoring both the urgency and the opportunity for businesses, policymakers, and innovators to accelerate high-integrity CDR.

14 January 2026: The Global Risks Report 2026, published ahead of Davos by the World Economic Forum (WEF), ranks geo-economic confrontation – the increasing use of economic tools such as trade restrictions, sanctions, tariffs, and control over critical resources as instruments of geopolitical power – as the most severe global risk of the coming decade, followed closely by biodiversity loss, underscoring the growing convergence of geopolitical and environmental instability.

Drawing on insights from over 1,300 experts, policymakers, and industry leaders worldwide, the report analyses global risks across three timeframes, helping decision-makers balance immediate crises with longer-term priorities while exploring the implications and interconnections of these risks. Extreme weather and biodiversity collapse sit at the centre of the 10-year global risk landscape.

The report argues that staying ahead of systemic climate risk will require forward-looking governance of AI and quantum technologies, large-scale investment in climate-resilient infrastructure, and social policies that reduce inequality and polarisation – ensuring climate action remains politically durable.

Headline News: EMEA (Europe, Middle East, & Africa)

20 March 2026: ENTSO-E, the European Network of Transmission System Operators for Electricity, which represents 40 electricity transmission system operators (TSOs) from 36 countries, published its Expert Panel’s final report on the 28 April 2025 blackout in continental Spain and Portugal.

The investigation concluded that the Iberian blackout – an unprecedented event – resulted from a combination of many interacting factors, including oscillations, gaps in voltage, and reactive power control, differences in voltage regulation practices, rapid output reductions, and generator disconnections in Spain, and uneven stabilisation capabilities. These factors led to fast increases of voltage and cascading generation disconnections in Spain, resulting in the blackout in continental Spain and Portugal.

Based on these findings, the Expert Panel sets out recommendations addressing each of the factors identified in the report to help prevent similar events in the future. These include strengthened operational practices, improved monitoring of system behaviour, and closer co-ordination and data exchange among power system actors. The findings of the investigation also underscore the need for regulatory frameworks to adapt in order to support the evolving nature of the power system.

If you have the fortitude, click here for the full 472-page 'Grid Incident in Spain and Portugal on 28 April 2025 ICS Investigation Expert Panel Final Report'.

10 March 2026: The Deploying CDR at Scale and Speed in Spain Roadmap, produced by Global Factor and Carbon Gap, was released, serving as a strategic guide for achieving carbon neutrality by 2050 through CDR.

Critical enablers are necessary to streamline the rollout, specifically a ‘one-stop’ permitting system to reduce investment uncertainty, and the creation of regional CO2 hubs that link multiple emission sources to shared storage. This approach requires fostered collaboration between government agencies, industry, and research institutions to align technical expertise with financing and strategic planning. Integrating these regional hubs into trans-European networks through frameworks like CEF Energy will further ensure that Spain’s domestic infrastructure remains competitive and aligned with broader European climate goals.

If these foundational elements are not set in motion this decade, the country risks a structural inability to deploy CDR, potentially leading to a costly dependence on foreign-controlled infrastructure. The report emphasises that Spain must treat this infrastructure as a matter of climate security and industrial strategy, rather than an optional undertaking, to safeguard the country’s economic sovereignty and long-term transition resilience in the face of increasing climate impacts.

Executive Insight: While the Spain Carbon Removal Roadmap offers a structured framework that can be adapted by other countries, it requires careful customisation to local conditions. Its methodological approach – assessing sectoral emissions gaps, evaluating CDR potential, and prioritising strategies – is broadly transferable, as are its phased planning model and stakeholder engagement processes. However, the specific strategies and recommendations in the roadmap reflect Spain’s unique energy mix, land use, climate, policies, and market conditions, which may differ significantly elsewhere. Other countries applying this roadmap would need to adjust targets, timelines, and approaches to account for local regulatory frameworks, infrastructure readiness, socio-economic factors, and public acceptance, ensuring that the roadmap functions as a practical guide rather than a one-size-fits-all solution.

20 January 2026: The UK published the National Security Assessment: Global Biodiversity Loss, Ecosystem Collapse report, developed by analysts across HM Government to inform long-term resilience planning.

The report examines how accelerating global biodiversity loss and ecosystem degradation directly threaten the UK’s stability, warning that the breach of planetary boundaries could intensify increasingly severe international security threats through cascading ecological, economic, and geopolitical impacts.

It highlights six ecologically vital regions, including the Amazon and South East Asian coral reefs, whose potential collapse could disrupt water and food supplies, trigger mass migration, and spark geopolitical tensions. Given the UK’s heavy reliance on imported food, these environmental shifts could realistically lead to significant resource scarcity and economic instability by 2030 and 2050.

To address these risks, the report calls for urgent ecosystem restoration and greater resilience in the global food system. It also identifies opportunities for innovation, green finance, and international collaboration to promote economic growth while safeguarding the ecosystems underpinning collective security and prosperity.

The assessment’s findings align closely with the WEF’s Global Risks Report 2026 (mentioned above), and evidence presented to national decision-makers at the National Emergency Briefing (NEB) on Climate and Nature presented to UK leaders in Westminster, London on 27 November 2025 (see more on the exciting evolution of this NEB call-to-action below).

19 January 2026: After concluding its 2024–2025 Climate and Nature Plan, the European Central Bank (ECB) is expanding its work on physical climate risks – the real economic effects of climate change, such as extreme weather events and long‑term shifts in climate patterns. To take a more comprehensive and forward-looking approach, the ECB is embedding both transition-related and physical climate risks more deeply into financial supervision and risk assessment processes.

A central move in this effort is the intensification of monitoring banks’ transition plans toward a green economy. The ECB will scrutinise how banks develop and implement strategies for sustainable operations, including how climate considerations are incorporated into their risk frameworks and operational practices.

Headline News: AMER (North, Central, & South America)

12 February 2026: The US Environmental Protection Agency (EPA) finalised a rule repealing its 2009 endangerment finding – the scientific and legal determination that GHG emissions endanger human health and welfare and therefore must be regulated under the Clean Air Act. Although the underlying science has not changed, the obligation to act on it has been rescinded, prompting immediate legal challenges from states, public health, scientific, and environmental organisations.

The original finding, grounded in extensive scientific analysis and upheld by courts, served as the legal foundation for federal climate policy for 16 years, requiring the regulation of CO2, methane, and other heat‑trapping pollutants, and enabling standards for vehicle emissions, power plants, and other major sources of GHGs. By overturning this determination, the EPA has effectively removed the federal obligation to regulate GHG pollution from extracting and burning fossil fuels, and simultaneously repealed emissions standards for light‑, medium‑ and heavy‑duty vehicles, fundamentally weakening the legal basis for climate protection in the US.

This shift has sweeping implications: it undermines longstanding federal climate safeguards, erases legal drivers for emissions reporting and limits, and exposes the American public to intensified climate impacts that are already affecting food systems, health outcomes, energy costs, and community infrastructure.

Executive Insight: The repeal creates new legal uncertainty for businesses, which may face shifting regulatory obligations and potentially increased litigation risk, as well as rising insurance costs to cover climate disaster recovery. For corporate executives, this underscores the urgent need to proactively manage climate risk, reinforce internal emissions governance, and ensure business strategies are resilient to both evolving US regulations and shifting global expectations.

7 January 2026: US President announced that the US would withdraw from a broad range of international climate, clean energy, sustainable development, and global cooperation organisations, including the landmark United Nations Framework Convention on Climate Change (UNFCCC). The Trump administration’s move would make the US the first country ever to pull out of the UNFCCC.

The presidential order also directs US agencies to disengage from other international bodies, including the Intergovernmental Panel on Climate Change (IPCC), the International Renewable Energy Agency (IRENA), and numerous climate, biodiversity, and sustainable development groups. While some of these withdrawals have already taken effect, treaty-based withdrawals such as the UNFCCC are subject to formal notice and a mandatory one-year waiting period, meaning full disengagement may not occur until early 2027.

This process is unfolding amid legal and political uncertainty. The UNFCCC was ratified by the US Senate in 1992, raising questions about whether a unilateral presidential withdrawal is permissible and potentially opening the door to court challenges or Congressional opposition. In the meantime, US agencies are gradually reducing participation, and the global community is closely monitoring both diplomatic and operational impacts.

Executive Insight: For businesses, this partial but unprecedented disengagement introduces both uncertainty and urgency, highlighting the importance of proactive strategies to navigate shifting international climate commitments.

Ten days after the announcement, on 27 January 2026, the US officially exited the Paris Agreement, one year after formally notifying the UN of its withdrawal as required under the treaty’s rules.

Headline News: APAC (Asia & Pacific)

Carbon & Climate Trends: Momentum on climate action across the APAC region continues to build, even amid global policy uncertainty. Increasingly, corporations are setting ambitious, science-based targets and enhancing transparency through structured disclosure frameworks. While Europe still leads in absolute numbers, APAC is steadily closing the gap, driven by a combination of regulatory developments, investor pressure, and the growing economic opportunity presented by clean technology deployment. This reflects a broader global trend: economic and technological drivers are maintaining forward progress in the energy transition, even when political headwinds persist.

Corporate engagement in APAC is deepening, with a rising share of companies committing to validated science-based targets. Disclosure of Scope 1, Scope 2, and increasingly Scope 3 emissions is expanding, demonstrating stronger alignment with climate strategies. Governments across the region are strengthening regulatory frameworks, including the adoption of ISSB-aligned reporting standards, embedding climate action into corporate governance and financial reporting. These institutional changes are encouraging both compliance and proactive investment in sustainability initiatives.

Investment in clean technology and renewable energy continues to grow, supported by strong venture and private capital flows. Solar, wind, and EV deployment are accelerating, highlighting the economic opportunity tied to the energy transition. However, the region remains heavily reliant on fossil fuels, and actual emissions reductions are uneven. While corporate commitments and clean-tech investment are rising, translating plans into measurable climate outcomes remains a key challenge for APAC markets.

28 January 2026: China continues to cement its position as a global leader in the energy transition, with an unprecedented scale of energy capacity expansion. Over the past four years, the country has added more power capacity than the entire existing grid of the United States, with solar accounting for more than half of new additions in the last year alone. This rapid build-out spans not only renewables but also wind, coal, and natural gas, reflecting a pragmatic, all-of-the-above approach to meeting surging energy demand. Alongside this infrastructure growth, China is also advancing climate governance. New voluntary climate disclosure rules introduced in late 2025 align closely with international standards while incorporating distinct features such as double materiality and links to national climate targets. These developments signal a dual focus on scaling clean energy and improving corporate transparency, positioning China as both a manufacturing and regulatory powerhouse in the low-carbon transition.

22 January 2026: India is emerging as a standout story in the global decarbonisation narrative, with evidence suggesting it may ‘leapfrog’ the traditional fossil-fuel-heavy development pathway. Analysis shows that at comparable stages of economic growth, India is adopting solar energy, electric vehicles, and electrification at a significantly faster pace than China did historically. Declining technology costs are a key enabler, allowing India to industrialise while avoiding the carbon-intensive detour taken by many developed economies. As the world’s most populous country and fastest-growing major economy, India’s trajectory has major implications for global emissions. Its ability to scale clean technologies quickly could become a defining factor in whether international climate targets remain within reach.

ICYMI: Coming to a Screen Near You

In Case You Missed It: The afore-mentioned National Emergency Briefing (NEB) was commissioned to present the latest evidence and build a call for the UK Government to stage a televised briefing as “the essential first step towards the WW2-scale response” we need to address the climate and nature crisis.

Now, combining expert insights from the original presentations with reactions from public figures and ordinary citizens, the NEB team has produced a 45-minute documentary specifically intended for community screenings. Dubbed The People’s Emergency Briefing, the film highlights how climate and nature crises are deeply interconnected with issues like public health, food security, economic stability, and national security – while also emphasising hopeful, practical actions that can lead to a better future.

As a campaign tool, it is designed to bring people, local groups, and decision-makers together, to spark meaningful, grassroots conversations and encourage audiences to take action, including signing an open letter calling on governments and broadcasters to respond to the climate and nature emergency with greater urgency.

Due for launch on 7 April 2026, screenings can be hosted in a wide variety of venues – from independent cinemas, arts centres, museums, and galleries to local settings such as village halls, libraries, schools, workplaces, and churches. More unconventional spaces – like cafés, pubs, or even outdoor locations – can also be used, making the film highly accessible to different communities.

Hosting a screening is straightforward. You secure a venue and date, invite a mix of stakeholders – including members of the public, local MPs, TDs, councillors, journalists, and other influential voices – and watch the film together, followed by a constructive, solution-focused discussion. NEB supports the entire process with a comprehensive Screening Guide and Supporter Toolkit.

While the film originated in the UK, its message is global. Climate change does not recognise borders, and both the challenges and solutions are shared. As an NEB Connector, EnergyElephant is proud to support this important conversation. If you’re keen to host a screening in your own community, simply register your interest, and the organisers will be in touch with more information.

If you found this post interesting, be sure to subscribe to our quarterly LinkedIn Newsletter. Our next Carbon Update will be published at the end of Q2 2026.